The Elephant in the Room

These days I am sure we are all paying attention to the nation’s recovery report card, the stock market’s daily mood swings, the price of gas, the staggering unemployment numbers, and oh yes, the foreclosure market that has been like a wild fire in the Southern California hills; it just keeps growing and spreading. The GDP appears strong at a fourth quarter annual growth rate of 5.7%, but home sales in December were down 7.6%. Does that make sense? Oh sure it does, because December is always a slow month for sales and there was that hiccup in the home buyer tax credit program. I’m not forgetting about unemployment, but why talk about it even though it is the biggest elephant in the room. Well, I guess we have to talk about it because our local flagship newspaper needs a sensational story to fill column inches.

Much to the displeasure of the real estate community, the Gazette once again decided to paint a most negative depressing picture about the real estate market, and the overall state of our union all in the name of truth penned by its resident editorial curmudgeon. The front page headline reads, “Foreclosures and Joblessness Up”. Sure we have about 24 bank owned properties in Dukes County that we are working to absorb, and there will surely be more on the way during this year. However, the writer insists on going on and on about the column inches all the foreclosures are taking up in print, and now we can put a number on unemployment predicting 50% over the next couple months, compared to about half that in normal times. With no new home starts, everyone counting pennies, only buying essentials and eating at home instead of going out to dinner, is this really breaking news?

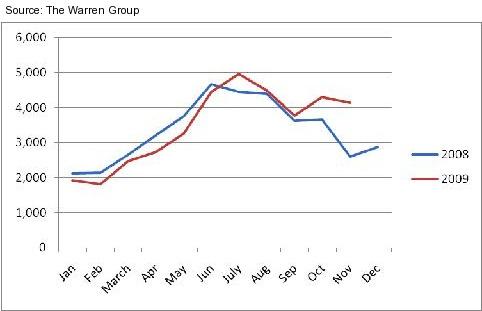

The good news in this editorial according to Chris Wells, president of MV Savings Bank is petitions to foreclose are not nearly what they are in the rest of Southern New England and the median sale prices in some towns actually increased from 2008 to 2009. West Tisbury shows a 2% increase and Edgartown a 14% increase in median sales prices. According to Mr. Wells, in the other three Island towns, Oak Bluffs was down 27%, Tisbury was down 19% and Chilmark saw the greatest reduction at 43% median sales price.

Martha’s Vineyard continues to bravely soldier on, its citizens doing all they can to make ends meet and keep a stiff upper lip. We have always been a hot and cold running Island with jobs for everyone during the tourist season and one of the highest, if not the highest unemployment rates in the Commonwealth for what amounts to 8 months during the off season. The Island greeting has become variations of “we’re hanging in there” and assurances that “we are all in this together”. Whew, I feel better already. What we all look for every day is some good news, news that will inspire us to keep on because we know summer is coming and with the sun we look forward to greeting all those visitors who love what Martha’s Vineyard has to offer, a simpler way of life. Oh by the way, bring your checkbook and support the Island economy.

Much to the displeasure of the real estate community, the Gazette once again decided to paint a most negative depressing picture about the real estate market, and the overall state of our union all in the name of truth penned by its resident editorial curmudgeon. The front page headline reads, “Foreclosures and Joblessness Up”. Sure we have about 24 bank owned properties in Dukes County that we are working to absorb, and there will surely be more on the way during this year. However, the writer insists on going on and on about the column inches all the foreclosures are taking up in print, and now we can put a number on unemployment predicting 50% over the next couple months, compared to about half that in normal times. With no new home starts, everyone counting pennies, only buying essentials and eating at home instead of going out to dinner, is this really breaking news?

The good news in this editorial according to Chris Wells, president of MV Savings Bank is petitions to foreclose are not nearly what they are in the rest of Southern New England and the median sale prices in some towns actually increased from 2008 to 2009. West Tisbury shows a 2% increase and Edgartown a 14% increase in median sales prices. According to Mr. Wells, in the other three Island towns, Oak Bluffs was down 27%, Tisbury was down 19% and Chilmark saw the greatest reduction at 43% median sales price.

Martha’s Vineyard continues to bravely soldier on, its citizens doing all they can to make ends meet and keep a stiff upper lip. We have always been a hot and cold running Island with jobs for everyone during the tourist season and one of the highest, if not the highest unemployment rates in the Commonwealth for what amounts to 8 months during the off season. The Island greeting has become variations of “we’re hanging in there” and assurances that “we are all in this together”. Whew, I feel better already. What we all look for every day is some good news, news that will inspire us to keep on because we know summer is coming and with the sun we look forward to greeting all those visitors who love what Martha’s Vineyard has to offer, a simpler way of life. Oh by the way, bring your checkbook and support the Island economy.

Labels: Bank owned properties, EXCLUSIVE Buyer Agency, Martha's Vineyard, Martha's Vineyard foreclosures, Peter Fyler, Real Estate Consumer Education, SplitRock Real Estate

posted by Peter C. Fyler, SplitRock Real Estate LLC at 2:18 PM

2 comments

![]()

-1a-741719.jpg)